Over time, as the benefit of these prepaid expenses is realized, the asset is reduced, and the expense is recognized. When doing your accounting journal entries, you are tracking how money moves in your business. Adjusting entries are the changes you make to these journal entries you’ve already made at the end of the accounting period.

How do adjusting entries affect financial statements?

To avoid this mistake, it is important to record transactions as soon as possible and ensure that they are accurate. To begin, the bookkeeper or accountant must identify the need for an adjustment entry. This could be due to an error in the original journal entry, the need to accrue expenses or revenue, or the need to record depreciation. In the accounting cycle, adjusting entries are made prior to preparing a trial balance and generating financial statements. For example, going back to the example above, say your customer called after getting the bill and asked for a 5% discount.

Accrual of Expenses

In other words, we are dividing income and expenses into the amounts that were used in the current period and deferring the amounts that are going to be used in future periods. The primary objective of accounting is to provide information that will help management take better decisions and plan for the future. It also helps users (lenders, employees and other stakeholders) to assess a business’s financial performance, financial position and ability to generate future Cash Flows. It has already been mentioned that it is essential to update and correct the accounting records to find the correct and true profit or loss of the business. Without adjusting entries to the journal, there would remain unresolved transactions that are yet to close.

Non-Cash Expenses

To avoid this mistake, it is important to keep track of all invoices and ensure that they are recorded accurately. Adjustment entries can also impact a business’s stock-based compensation expenses. For example, if an adjustment entry is made to increase the fair value of stock options that were granted to employees, this will increase the amount of compensation expense that the business records. The revenue recognition principle requires businesses to recognize revenue when it is earned, regardless of when payment is received. Adjustment entries are necessary to ensure that revenue is recognized in the correct period, even if payment has not been received.

- The actual cash transaction would still be tracked in the statement of cash flows.

- Adjustment entries are an important tool for businesses to ensure that their financial statements are accurate.

- At the end of each accounting period, businesses need to make adjusting entries.

Types of Adjustment Entries

Then, when you get paid in March, you move the money from accrued receivables to cash. If you have a bookkeeper, you don’t need to worry about making your own adjusting entries, or referring to them while preparing financial statements. In August, you record that money in accounts receivable—as income you’re expecting to receive. Then, in September, you record the money as cash deposited in your bank account.

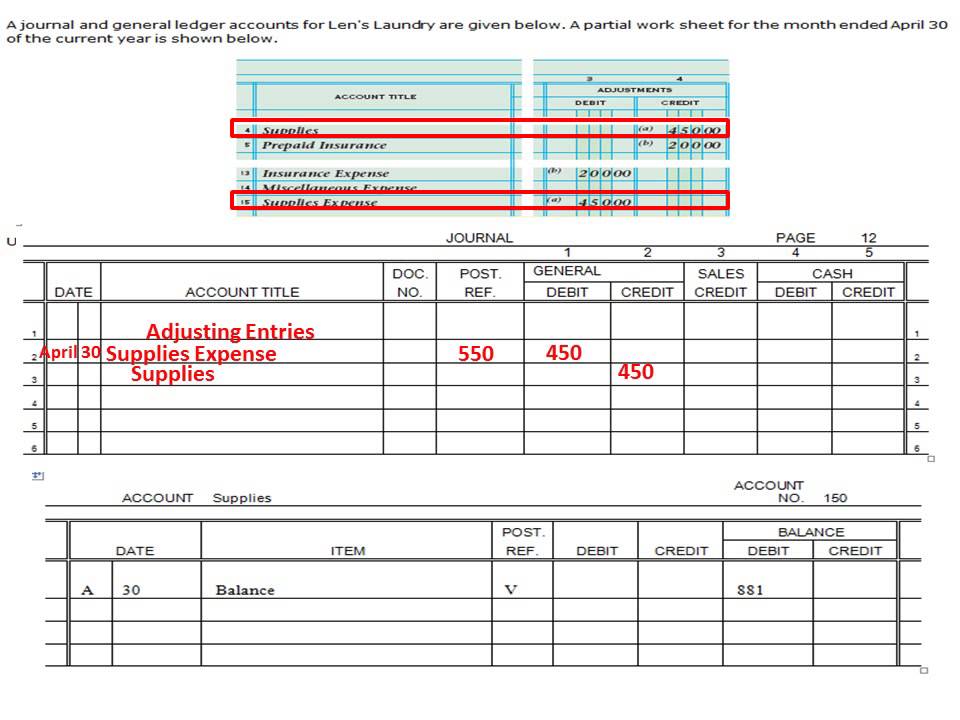

Accrued expenses are expenses made but that the business hasn’t paid for yet, such as salaries or interest expense. At the end of each accounting period, businesses need to make adjusting entries. A related account is Insurance Expense, which appears on the income statement. The amount in the Insurance Expense account should report the amount of insurance expense expiring during the period indicated in the heading of the income statement. This can happen when invoices are not properly recorded or when estimates are not updated.

Under this arrangement December’s interest expense will be paid in December, January’s interest expense will be paid in January, etc. You simply record the interest payment and avoid the need for an adjusting entry. Similarly, your insurance company might automatically charge your company’s checking account each month for the insurance expense that applies to just that one month. An adjusting journal entry is an entry in a company’s general ledger scaled agile inc unveils safe® enterprise that records transactions that have occurred but have not yet been appropriately recorded in accordance with the accrual method of accounting. The entry records any unrecognized income or expenses for the accounting period, such as when a transaction starts in one accounting period and ends in a later period. Adjusting entries are accounting journal entries that convert a company’s accounting records to the accrual basis of accounting.

The process of recording adjustment entries involves making changes to the general ledger accounts to correct errors or to account for transactions that were not recorded during the regular accounting cycle. Adjustment entries are accounting entries made at the end of an accounting period to record transactions that have occurred but have not yet been recorded. These entries are necessary to ensure that financial statements accurately reflect the company’s financial position and performance. Depreciation is the process of allocating the cost of a tangible fixed asset over its useful life. This type of adjusting entry ensures that the expense of using the asset is matched with the revenue it generates over time. For example, if a company purchases machinery for $100,000 with an expected useful life of 10 years, an annual depreciation expense of $10,000 would be recorded.

Now that all of Paul’s AJEs are made in his accounting system, he can record them on the accounting worksheet and prepare an adjusted trial balance. Adjusting Entries reflect the difference between the income earned on Accrual Basis and that earned on cash basis. This enables us to arrive at the true result of business activities for a given period (e.G., Whether we made profits or suffered losses). The number and variety of adjustments needed at the end of the accounting period differ depending on the size and nature of the business.

The updating/correcting process is performed through journal entries that are made at the end of an accounting year. Similarly, under the realization concept, all expenses incurred during the current year are recognized as expenses of the current year, irrespective of whether cash has been paid or not. Also, according to the realization concept, all revenues earned during the current year are recognized as revenue for the current year, regardless of whether cash has been received or not. Before exploring adjusting entries in greater depth, let’s first consider accounting adjustments, why we need adjustments, and what their effects are. Accruals refer to payments or expenses on credit that are still owed, while deferrals refer to prepayments where the products have not yet been delivered.